Did you inherit real estate property but you cannot transfer it under your name because of unpaid taxes?

Avail now of the Estate Tax Amnesty in the Philippines!

Mga Benepisyo (Benefits):

- 6% tax lang ang babayaran ! (You will only pay 6% )

- Walang babayarang back taxes at penalties (You will not pay back taxes and penalties.)

- Absuwelto pa sa demanda!

Republic Act No. 11213 (RA 11213) or the Tax Amnesty Act aims

“to provide the taxpayers a one-time opportunity to settle estate tax obligations through an estate tax amnesty program that will give reasonable tax relief to estates with outstanding estate tax liabilities.”

Working with the Philippines’ Tax Collecting Agency, I have noted that a lot of Filipinos are owning properties under the name of their deceased parents or ancestors. Most of them were not able to properly transfer the properties under their name because of the unpaid estate tax and the incurred penalties.

June 15, 2019 and, is the start of the two-year period provided for by Republic Act 11213 (RA 11213) or the “Tax Amnesty Act” within which the taxpayers can avail themselves of the benefits of the Estate Tax Amnesty law. I wrote the basics of the Estate Tax Amnesty Act

here but for a more detailed clarification on issues, here are 40 Frequently Asked Questions on the Estate Tax Amnesty 2019 in the Philippines.

Q1: Who is qualified to avail of the estate tax amnesty under RA No. 11213?

A1:The estate of the decedent who died on or before December 31, 2017, who is not covered by the exceptions enumerated under Sec. 3 of RR No. 6-2019 dated May 29,2019, is qualified to avail of tax amnesty.

Q2: Who shall file the estate tax amnesty?

A2: The executor or administrator, legal heirs, transferees or beneficiaries (or filer) shall file the estate tax amnesty return within two (2) years from the effectivity of RR No. 6-2019 or from June 15, 2019 to June 14, 2021.

Q3: Will a Taxpayer Identification Number (TIN) be issued for the estate of the decedent?

A3: Yes, if there is no existing TIN.

Q4: Are all heirs required to secure their own TIN?

A4: Yes, all heirs, including minors without TIN are required to secure their respective TIN.

Q5: What BIR form will be used in the filing and payment of estate tax amnesty?

Q6: When and where will the ETAR be filed?

A6: The ETAR shall be filed with the Revenue District Office (RDO) having jurisdiction over the last residence of the decedent, within two (2) years from the effectivity of RR No. 6-2019 or from June 15, 2019 to June 14, 2021. In case the estate has a previously issued TIN, the ETAR shall be filed with the RDO which issued the said TIN.

For non-resident decedent, the executor or administrator in the Philippines, shall file the return with the RDO where such executor/administrator is registered or if not yet registered, at the RDO having jurisdiction over the legal residence of the executor/administrator. If there is no executor or administrator, the return shall be filed with RDO No. 39-South Quezon City.

If the properties involved are common properties of multiple decedents emanating from the first decedent, and no estate tax returns have been previously filed, the amnesty tax returns for every stage of transfer/succession may be filed together in any one (1) RDO having jurisdiction over the last residence of any of the decedents.

Illustration:

How to file estate of decedents involving several stages of succession from a common property left by the first decedent

| Stage of Succession | Property | Decedent | Date of Death | Last Residence | Where to file |

|---|

| 1st | TCT No. 12345 | Alpha | Dec. 31, 1985 | Caloocan City | All four (4) ETARS may be filed in any of the RDOs covering the last residence of any of the decedent |

| 2nd | TCT No. 12345 | Bravo

(heir of Alpha) | July 27, 1992 | Cabanatuan City, Nueva Ecija | All four (4) ETARS may be filed in any of the RDOs covering the last residence of any of the decedent |

| 3rd | TCT No. 12345 | Charlie

(heir of Bravo) | Dec. 31, 1997 | Calbayog City,Samar | All four (4) ETARS may be filed in any of the RDOs covering the last residence of any of the decedent |

| 4th | TCT No. 12345 | Delta

(heir of Charlie) | Dec. 31, 2017 | Tagum City, Davao Del Norte | All four (4) ETARS may be filed in any of the RDOs covering the last residence of any of the decedent |

Q7: Where will the ETAR be filed if the estate has a previously issued TIN?

A7: The ETAR shall be filed with the RDO which issued the said TIN

Q8: How many ETAR shall be filed?

A8: One (1) ETAR in triplicate copies shall be filed for the estate of every decedent.

- Original – Document Processing Division (DPD)

- Duplicate – Docket File

- Triplicate – Taxpayer’s Copy

Q9: Can the estate tax amnesty application be filed through eBIR facility?

A9: No. The forms are downloadable from the BIR website and are not available in eBIRForms. Hence, the filing and payment of estate tax amnesty shall be done manually.

involves multiple decedents?

A10: One (1) EJS for every stage of transfer/succession or one (1) EJS covering all the stages of transfer/succession with respect to the inherited share of the common property/ies emanating from the first decedent shall be submitted.

Q11: When no zonal valuation is available at the time of death, what will be used as reference for

purposes of valuation of properties?

A11: The Fair Market Value (FMV) appearing in the tax declaration issued at the date of death or the succeeding available tax declaration issued nearest to the date of death shall be used as reference in computing the value of the property at the time of death.

Q12: Will the filer be required to submit certificate of zonal valuation from the RDO

where the property is located?

A12: No. Verification of zonal values can be made thru the

BIR website.

Q13: If there is no tax declaration available at the time of death, what will be used as

basis to comply with the requirement?

A13: The succeeding available tax declaration issued nearest to the date of death shall be used as reference.

Q14: What will be the estate tax amnesty rate? Is there a minimum amount to be paid to

avail of the estate tax amnesty?

A14: A rate of six percent (6%) based on the decedent’s total net taxable estate at the time of death shall be imposed at every stage of succession. The minimum amount is Five Thousand Pesos (P5,000.00).

Q15: What is the basis in computing the estate tax amnesty due on undeclared properties

for the previously filed estate tax return?

A15: An estate tax amnesty rate of six percent (6%) shall be imposed on the value of the undeclared properties at the time of death, without deductions which are deemed to have been claimed in the previous estate tax return filed, except for the share of the surviving spouse on the undeclared conjugal property. However, in no case shall the payment be lower than Five Thousand Pesos (P5,000.00).

Example No. 1. Mr. X died on June 30, 2017. After filing the estate tax return under BIR Form 1801 on November 15, 2017, the heirs discovered that a conjugal real property with FMV of P3,000,000.00 was not included in the gross estate declared.

Since there is an estate tax return previously filed, an estate amnesty amount of P90,000.00, after deducting the share of surviving spouse, shall be computed as follows:

| FMV of the property | 3,000,000.00 |

|---|

| Less: Share of surviving spouse | 1,500,000.00 |

| Net undeclared property | 1,500,000.00 |

| Multipy by | 6% |

| Estate Tax Amnesty Amount Due | 90,000.00 |

Example No. 2. Mr. X died on June 30, 2017. Since no estate tax return has been previously filed, the heirs availed of the estate tax amnesty on June 26, 2019. After a few months, the heirs discovered that a conjugal real property with FM of P3,000,00.00 was not included in the gross estate declared.

Since there is an ETAR previously filed, the amount of P90,000.00, after deducting the share of surviving spouse, shall be computed as follows:

| FMV of the property | 3,000,000.00 |

|---|

| Less: Share of surviving spouse | 1,500,000.00 |

| Net undeclared property | 1,500,000.00 |

| Multipy by | 6% |

| Estate Tax Amnesty Amount Due | 90,000.00 |

Q16: Can the filer still avail of the estate tax amnesty for undeclared property if the estate

has an existing estate tax delinquency?

A16: Yes, provided that the undeclared property is not included in the list of properties covered in the existing estate tax delinquency. Further, the ETAR shall be filed in the RDO that issued the assessment.

Q17: The basic estate tax due of a decedent who died on December 31, 2017 was voluntarily

paid on August 15, 2018, but the taxpayer failed to pay the corresponding penalties.

Can the taxpayer avail of the estate tax amnesty on the unpaid penalties?

A17: Yes, by paying the minimum estate tax amnesty amount of Five Thousand Pesos (P5,000.00) and filing the required ETAR.

Q18: When will the APF be approved and endorsed for payment by the Revenue District Officer?

A18: The APF shall be approved and endorsed by the Revenue District Officer for payment after the pre-evaluation of the complete documentary requirements submitted by the filer and upon computation of the estate tax amnesty due.

Q19: Where will the estate tax amnesty be paid and what document shall be presented

for payment?

A19: Payment shall be made to any Authorized Agent Bank (AAB) under the jurisdiction of the concerned RDO by presenting the duly endorsed APF.

However, payment may be made to the Revenue Collection Officer (RCO) under the following instances:

- In case of cash payment and the amount involved is Twenty Thousand Pesos (P20,000.00) and below; and

- If the payment is through manager’s/cashier’s check, irrespective of amount.

If there is no AAB in the RDO, payment shall be made to the RCO subject to the conditions in”1″ and “2” above.

Q20: Will the BIR allow a partial or total withdrawal of cash in bank for payment

of estate tax amnesty?

A20: The Commissioner or the Revenue District Officer may, upon written request of the taxpayer, issue a letter allowing partial or total withdrawal of the cash equivalent to the estate tax amnesty due without subjecting to the final withholding tax.

The form of payment to be issued by the bank should be a manger’s/cashier’s check which shall indicate in the space provided for “PAY TO THE ORDER OF”:

- presenting/collecting bank or the bank where the payment is to be coursed and

- FAO (For the Account of) Bureau of Internal Revenue as payee.

Q21: Can the estate tax amnesty be paid in installment?

A21: No. For purposes of estate tax amnesty, installment payment is not allowed.

Q22: Do we compute both estate and inheritance taxes in case the decedent died at

the time when there were estate and inheritance taxes imposed?

A22: No. The estate tax amnesty rate of six percent (6%), which shall cover both the unpaid estate and inheritance taxes, shall be computed based on the net taxable estate.

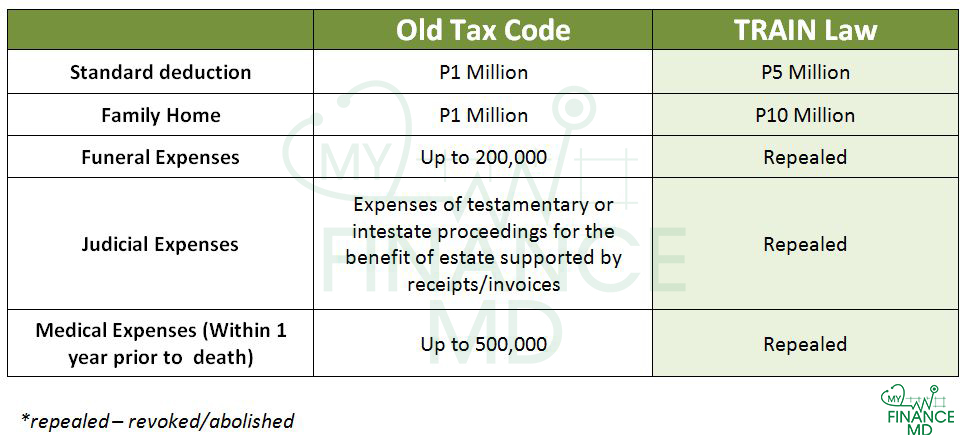

Q23: What are the deductions to be applied in the computation of net taxable estate?

A23: The deductions to be applied in the estate tax amnesty shall be based on the estate tax law prevailing at the time of death.

Click to view Allowable Deductions from the Gross Estate

Q24: Can the estate involving judicial settlement/last will of testament pending in court

avail the estate tax amnesty?

A24: Yes, provided that the filer shall submit a certified true copy of the court resolution or leave of court together with all the documentary requirements for estate tax amnesty within the two-year availment period. However, only the CA shall be issued on the filer.

The ONETT Team of the RDO who will prepare the CA shall encode the details of the property/ies listed in the inventory of properties/last will of testament pending in court on the lower portion of the CA after the caveat or at the back of the CA.

Q25: In relation to Q24, when will the electronic Certificate Authorizing Registration

(eCAR) be issued?

A25: The eCAR shall be issued upon presentation of the final order of the court.

Q26: If there is an on-going expropriation case on the property, can the taxpayer avail

of the estate tax amnesty?

A26: Yes. If the expropriation happened after the death of the decedent, the expropriated property will form part of the gross estate of the decedent and can avail of the amnesty. However, if the expropriation happened during the lifetime of the decedent, the expropriated property will not form part of the gross estate of the decedent.

Q27: In case of multiple succession, how will the names of the estates and corresponding

heirs be presented on the eCAR?

A27: All the names of the decedents as stated on EJS or Judicial Settlement, as the case may be, will be shown on the eCAR. A brief explanation as to consolidation of the estates and the corresponding payment for all estates must be clearly stated on the “Remarks” and “Payment Details” fields, of the eCAR, respectively.

Q28: How many eCARS shall be issued for a real property covered by one (1) Title

involving multiple succession?

A28: One (1) eCAR only will be issued per real property, including the improvements, if any, provided that the eTARS are filed simultaneously at only one (1) RDO.

Q29: Is delinquent estate tax liability covered on the RR on Estate Tax Amnesty?

A29: No. It is covered by Sec. 3 of RR No. 4-2019 on tax amnesty on delinquencies, quoted hereunder:

“SECTION 3. COVERAGE. All persons, whether, natural or juridical, with internal revenue tax liabilities covering taxable year 2017 and prior years, may avail of Tax Amnesty on Delinquencies within one (1) year from the effectivity of these Regulations, under any of the following instances:

A. Delinquent Accounts as of the effectivity of these Regulations, including the following:

- Delinquent Accounts with application of compromise settlement either on the basis of (a) doubtful validity of the assessment or (b) financial incapacity of the taxpayer, whether the same was denied by or still pending with the Regional Evaluation Board (REB) or the National Evaluation Board (NEB), as the case may be, on or before the effectivity of these Regulations;

- Delinquent Withholding Tax liabilities arising from non-withholding of tax; and

- Delinquent Estate Tax liabilities.”

Q30: Can the estate still avail of the tax amnesty if the filer failed to submit

the validated APF with proof of payment to the concerned RDO within the two-year

availment period of tax amnesty?

A30: No. Failure to submit the validated APF with proof of payment within the two-year period from the effectivity of RR No. 6-2019 is tantamount to non-availment of the Estate Tax Amnesty. However, any payment made may be applied against the total regular estate tax due inclusive of penalties.

Q31: The decedent died on December 20, 2017. The corresponding estate tax return

indicating estate tax due of P500,000.00 was filed on May 15, 2018 but only P350,000.00

was paid. Can the taxpayer avail of estate tax amnesty for the unpaid tax due?

A31: Yes, the filer can avail the tax amnesty on the difference between the net taxable estate per original declaration and net taxable estate applicable to the estate tax amount paid, computed using the applicable scheduled rates, as presented below:

| | Per Return |

|---|

| Gross Estate | | 7,933,333.35 |

| Less: Allowable Deductions | | |

| Funeral Expense | 200,000.00 | |

| Medical Expense | 500,000.00 | |

| Family Home | 1,000,000.00 | 2,700,000.00 |

| Standard Deduction | 1,000,000.00 | 5,233,333.35 |

| Total Net Estate | | 0.00 |

| Less: Share of Surviving Spouse (assuming none) | | 5,233,333.35 |

| Net Taxable Estate (with estate tax due of P500,000.00) | | |

Net Taxable Estate applicable to the paid P350,000.00

Taxable Estate:

Applicable to P135,000.00 | 2,000,000.00 | |

Applicable to Excess

(P350,000-P135,00)/11% | 1,954,545.45 | |

| 3,954,545.45 | 3,954,545.45 |

| Net Taxable Estate subject to tax amnesty | | 1,278,787.90 |

| Estate Tax Amnesty Due (6%) | | 76,727.27 |

The ETAR shall be filed in the same RDO where the estate tax return was filed and the following documents shall be presented:

- Copy of Estate Tax Return previously filed; and

- Certificate of Payment from the RDO if available, otherwise, secure from Revenue Accounting Division (RAD) in the National Office.

Q32: Using the same facts on Q31, after the taxpayer paid the estate tax amnesty

amounting to P76,727.27 as computed, it was later on discovered that a certain real

property owned by the decedent with FMV per tax declaration of P1,500,000.00

and ZV of P1,000,000.00 (no improvement) was not declared in the previously filed

ETAR. Can the taxpayer still avail of the estate amnesty on the undeclared

property and what would be the estate tax amnesty amount?

A32: Yes, the estate tax amnesty due is 6% of P1,500,000.00, which is the higher value between FMV and ZV of the undeclared real property.

Q33: If the undeclared property on Q32 is a conjugal property, how much is the

estate tax amnesty amount?

A33: The estate tax amnesty amount shall be computed as follows:

| FMV of the property | 1,500,000.00 |

| Less: Share of surviving spouse | 750,000.00 |

| Net undeclared property | 750,000.00 |

| Multiply by | 6% |

| Estate Tax Amnesty Amount Due | 45,000.00 |

Q34: Will the withdrawal from the bank of the estate be allowed after presentation

of the Certificate of Availment only?

A34: No. Withdrawal can only be allowed upon presentation of the eCAR, except when a written request allowing partial or total withdrawal of cash of the taxpayer was approved by the Commissioner or the Revenue District Officer.

Q35: What document will be submitted in case there is no death certificate issued

by the Philippine Statistics Authority (PSA)?

A35: The Certificate of No Record of Death from PSA and any valid secondary evidence including but not limited to those issued by any government agency/office sufficient to establish the fact of death of the decedent may be submitted.

Q36: Can the filer avail of the estate tax amnesty if there is an on-going investigation

on estate tax liabilities?

A36: Yes, since there in no estate tax due that is considered delinquent.

Q37: Can the taxpayer avail of the estate tax amnesty on the estate tax deficiency

resulting from post review made by the Assessment Division?

A37: Yes, the taxpayer can avail of the estate tax amnesty.

Q38: Formal Assessment Notice (FAN) covering deficiency estate tax was issued

against the estate of X who died on December 31, 2017. Within thirty (30) days

from receipt of the FAN, the heirs of X filed a valid protest. Can the heirs of X

avail of the estate tax amnesty?

A38: Yes, the heirs can avail of the estate tax amnesty since the deficiency estate tax assessment is not yet considered delinquent.

Q39: Can the holder/buyer in a deed of sale transaction avail of the estate tax

amnesty on behalf of the heirs?

A39: Yes, provided that the holder/buyer shall present the notarized EJS signed by all heirs together with complete documentary requirements.

Q40: Will the voluntary payment made under Payment Form No. 0605, supposedly

for estate tax amnesty, prior to the effectivity of RR No. 6-2019 be considered as valid

payment for amnesty?

A40: No, because at the time of payment, the estate tax amnesty is not yet effective. Moreover, the proper form for amnesty payment is BIR Form No. 0621-EA – APF which must be duly approved and endorsed by the concerned Revenue District Officer.

The voluntary payment in this case may be claimed for refund subject to existing rules and regulations on refund.

Source: RMC 68-2019